Deterministic Production Adjustment Model

Contents

Deterministic Production Adjustment Model¶

Randall Romero Aguilar, PhD

This demo is based on the original Matlab demo accompanying the Computational Economics and Finance 2001 textbook by Mario Miranda and Paul Fackler.

Original (Matlab) CompEcon file: demdoc05.m

Running this file requires the Python version of CompEcon. This can be installed with pip by running

!pip install compecon --upgrade

Last updated: 2021-Oct-01

About¶

Profit maximizing firm must decide how rapidly to adjust production.

State

q current production rate

Control

x production adjustment rate

Parameters

𝛼 production cost constant

β production cost elasticity

γ adjustment cost parameters

p price

𝜌 continuous discount rate

Preliminary tasks¶

Import relevant packages¶

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from compecon import BasisChebyshev, OCmodel, NLP

Model parameters¶

𝛼 = 1.0 # production cost constant

β = 1.5 # production cost elasticity

γ = 4.0 # adjustment cost parameters

p = 1.0 # price

𝜌 = 0.1 # continuous discount rate

Approximation structure¶

n = 10 # number of basis functions

qmin = 0.2 # minimum state

qmax = 0.7 # maximum state

basis = BasisChebyshev(n, qmin, qmax, labels=['x']) # basis functions

Steady-state¶

qstar = (p/(𝛼*β)) ** (1/(β-1))

xstar = 0

vstar = (p * qstar - 𝛼 * qstar**β)/𝜌

steadystate = pd.Series([qstar, xstar],

index=['Production', 'Production adjustment rate'])

steadystate

Production 0.444444

Production adjustment rate 0.000000

dtype: float64

Solve HJB equation by collocation¶

def control(q, Vq, 𝛼, β, γ, p, 𝜌):

return Vq / γ

def reward(q, x, 𝛼, β, γ, p, 𝜌):

k = 𝛼 * q ** β

a = 0.5 * γ * x**2

return p*q - k - a

def transition(q, x, 𝛼, β, γ, p, 𝜌):

return x

model = OCmodel(basis, control, reward, transition, rho=𝜌, params=[𝛼, β, γ, p, 𝜌])

data = model.solve()

Solving optimal control model

iter change time

------------------------------

0 1.3e+00 0.0030

1 8.8e-02 0.0030

2 4.1e-02 0.0040

3 1.6e-02 0.0040

4 3.4e-03 0.0040

5 1.9e-04 0.0050

6 6.2e-07 0.0050

7 1.2e-11 0.0060

Elapsed Time = 0.01 Seconds

Plots¶

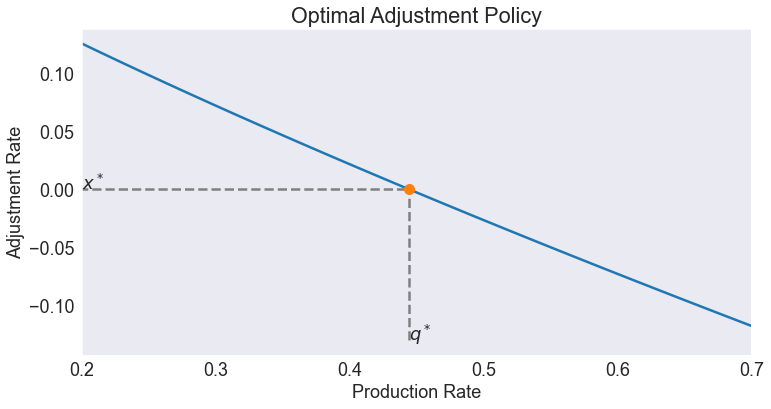

Optimal policy¶

fig, ax = plt.subplots()

data['control'].plot(ax=ax)

ax.set(title='Optimal Adjustment Policy',

xlabel='Production Rate',

ylabel='Adjustment Rate',

xlim=[qmin, qmax])

lb = ax.get_ylim()[0]

ax.hlines(xstar, 0, qstar, colors=['gray'], linestyles=['--'])

ax.vlines(qstar, lb, xstar, colors=['gray'], linestyles=['--'])

ax.annotate('$x^*$', (qmin, xstar))

ax.annotate('$q^*$', (qstar, lb))

ax.plot(qstar, xstar, '.', ms=20);

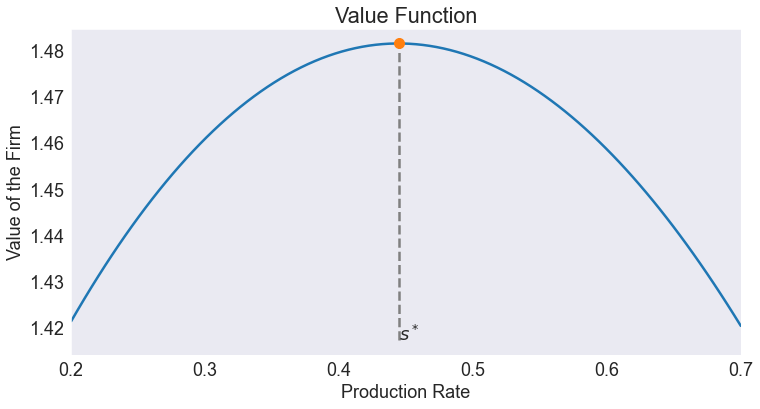

Value function¶

fig, ax = plt.subplots()

data['value'].plot(ax=ax)

ax.set(title='Value Function',

xlabel='Production Rate',

ylabel='Value of the Firm',

xlim=[qmin, qmax])

lb = ax.get_ylim()[0]

ax.vlines(qstar, lb , vstar, colors=['gray'], linestyles=['--'])

ax.annotate('$s^*$', (qstar, lb))

ax.plot(qstar, vstar, '.', ms=20);

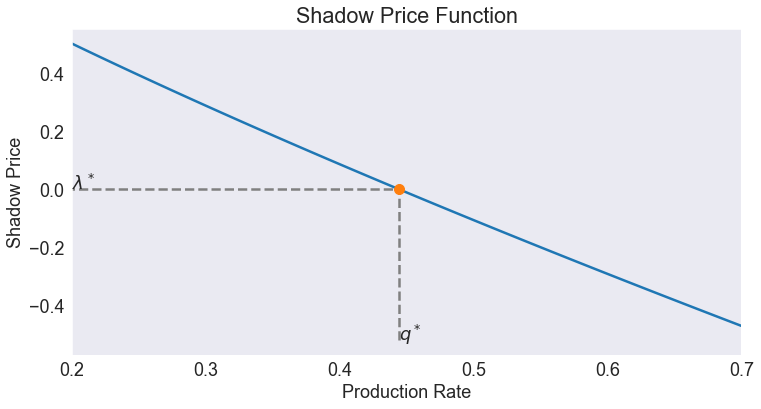

Shadow price¶

data['shadow'] = model.Value(data.index, 1)

fig, ax = plt.subplots()

data['shadow'].plot(ax=ax)

ax.set(title='Shadow Price Function',

xlabel='Production Rate',

ylabel='Shadow Price',

xlim=[qmin, qmax])

pstar = model.Value(qstar, 1)

lb = ax.get_ylim()[0]

ax.hlines(pstar, 0, qstar, colors=['gray'], linestyles=['--'])

ax.vlines(qstar, lb , pstar, colors=['gray'], linestyles=['--'])

ax.annotate('$\lambda^*$', (qmin, pstar))

ax.annotate('$q^*$', (qstar, lb))

ax.plot(qstar, pstar, '.', ms=20);

Residual¶

fig, ax = plt.subplots()

ax.axhline(0, c='white')

data['resid'].plot(ax=ax)

ax.set(title='HJB Equation Residual',

xlabel='Production Rate',

ylabel='Residual',

xlim=[qmin, qmax]);

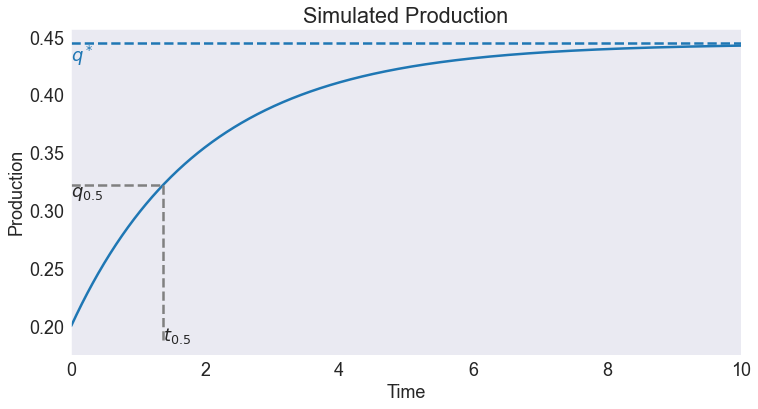

Simulate the model¶

Initial state and time horizon¶

q0 = 0.2 # initial production

T = 10 # time horizon

Simulation and plot¶

fig, ax = plt.subplots()

simulation = model.simulate([[q0]], T)

# Time to midway adjustment

qhalf = (q0 + qstar)/2

thalf = np.interp(qhalf, simulation['$y_0$'], simulation.index)

simulation['$y_0$'].plot(ax=ax)

ax.set(title='Simulated Production',

xlabel='Time',

ylabel='Production',

xlim=[0, T],

xticks=np.arange(0,T+1,2))

ax.axhline(qstar, ls='--', c='C0')

ax.annotate('$q^*$', (0, qstar), color='C0', va='top')

lb = ax.get_ylim()[0]

ax.vlines(thalf, lb , qhalf, colors=['gray'], linestyles=['--'])

ax.hlines(qhalf, 0 , thalf, colors=['gray'], linestyles=['--'])

ax.annotate('$t_{0.5}$', (thalf, lb))

ax.annotate('$q_{0.5}$', (0, qhalf),va='top')

ax.legend([]);

PARAMETER xnames NO LONGER VALID. SET labels= AT OBJECT CREATION