Stochastic Optimal Economic Growth Model

Contents

Stochastic Optimal Economic Growth Model¶

Randall Romero Aguilar, PhD

This demo is based on the original Matlab demo accompanying the Computational Economics and Finance 2001 textbook by Mario Miranda and Paul Fackler.

Original (Matlab) CompEcon file: demdp07.m

Running this file requires the Python version of CompEcon. This can be installed with pip by running

!pip install compecon --upgrade

Last updated: 2022-Oct-23

About¶

Welfare maximizing social planner must decide how much society should consume and invest. Unlike the deterministic model, this model allows arbitrary constant relative risk aversion, capital depreciation, and stochastic production shocks. It lacks a known closed-form solution.

States

s stock of wealth

Actions

k capital investment

Parameters

ɑ relative risk aversion

β capital production elasticity

ɣ capital survival rate

σ production shock volatility

δ discount factor

import numpy as np

import matplotlib.pyplot as plt

from compecon import BasisChebyshev, DPmodel, DPoptions, qnwlogn

import seaborn as sns

import pandas as pd

Model parameters¶

α, β, γ, σ, δ = 0.2, 0.5, 0.9, 0.1, 0.9

Analytic results¶

The deterministic steady-state values for this model are

kstar = ((1 - δ*γ)/(δ*β))**(1/(β-1)) # steady-state capital investment

sstar = γ*kstar + kstar**β # steady-state wealth

Numeric results¶

State space¶

The state variable is s=”Wealth”, which we restrict to \(s\in[5, 10]\).

Here, we represent it with a Chebyshev basis, with \(n=10\) nodes.

n, smin, smax = 10, 5, 10

basis = BasisChebyshev(n, smin, smax, labels=['Wealth'])

Continuous state shock distribution¶

m = 5

e, w = qnwlogn(m, -σ**2/2,σ**2)

Action space¶

The choice variable k=”Investment” must be nonnegative.

def bounds(s, i=None, j=None):

return np.zeros_like(s), 0.99*s

Reward function¶

The reward function is the utility of consumption=\(s-k\).

def reward(s, k, i=None, j=None):

sk = s - k

u = sk**(1-α) / (1-α)

ux= -sk **(-α)

uxx = -α * sk**(-1-α)

return u, ux, uxx

State transition function¶

Next period, wealth will be equal to production from available initial capital \(k\), that is \(s' = k^\beta\)

def transition(s, k, i=None, j=None, in_=None, e=None):

g = γ * k + e * k**β

gx = γ + β*e * k**(β-1)

gxx = β*(β-1)*e * k**(β-2)

return g, gx, gxx

Model structure¶

The value of wealth \(s\) satisfies the Bellman equation

To solve and simulate this model,use the CompEcon class DPmodel

growth_model = DPmodel(basis, reward, transition, bounds,e=e,w=w,

x=['Investment'],

discount=δ )

Solving the model¶

Solving the growth model by collocation.

S = growth_model.solve()

Solving infinite-horizon model collocation equation by Newton's method

iter change time

------------------------------

0 8.2e+00 0.0000

1 9.6e+00 0.0781

2 2.2e+00 0.1250

3 3.8e-02 0.1718

4 7.0e-06 0.2030

5 7.1e-15 0.2191

Elapsed Time = 0.22 Seconds

DPmodel.solve returns a pandas DataFrame with the following data:

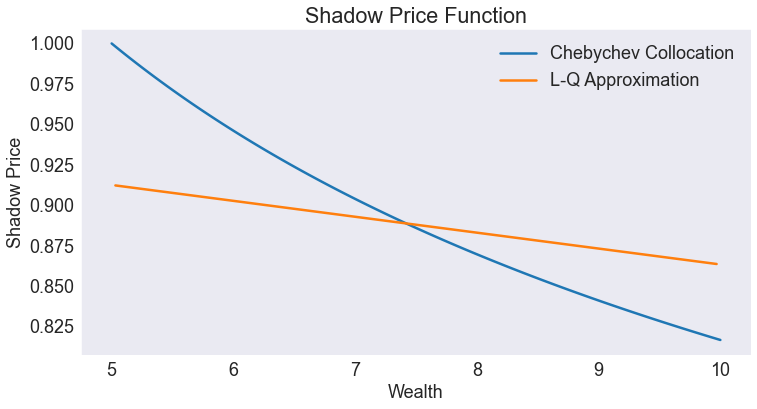

We are also interested in the shadow price of wealth (the first derivative of the value function).

To analyze the dynamics of the model, it also helps to compute the optimal change of wealth.

S['shadow price'] = growth_model.Value(S['Wealth'],1)

S['D.Wealth'] = transition(S['Wealth'], S['Investment'],e=1)[0] - S['Wealth']

S.head()

| Wealth | value | resid | Investment | shadow price | D.Wealth | |

|---|---|---|---|---|---|---|

| Wealth | ||||||

| 5.000000 | 5.000000 | 17.793592 | 4.324104e-09 | 3.997670 | 0.999535 | 0.597321 |

| 5.050505 | 5.050505 | 17.843995 | -1.837417e-09 | 4.032514 | 0.996440 | 0.586869 |

| 5.101010 | 5.101010 | 17.894243 | -4.078490e-09 | 4.067300 | 0.993391 | 0.576314 |

| 5.151515 | 5.151515 | 17.944339 | -3.954334e-09 | 4.102028 | 0.990386 | 0.565657 |

| 5.202020 | 5.202020 | 17.994283 | -2.583509e-09 | 4.136700 | 0.987425 | 0.554898 |

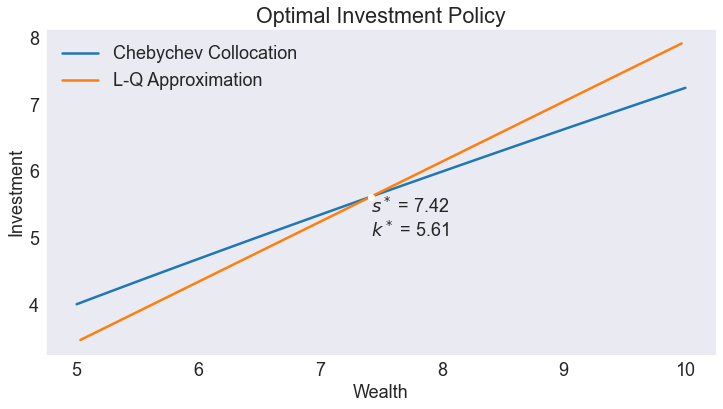

Solving the model by Linear-Quadratic Approximation¶

The DPmodel.lqapprox solves the linear-quadratic approximation, in this case arround the steady-state. It returns a LQmodel which works similar to the DPmodel object. We also compute the shadow price and the approximation error to compare these results to the collocation results.

growth_lq = growth_model.lqapprox(sstar, kstar)

L = growth_lq.solution(basis.nodes)

L['shadow price'] = L['value_Wealth']

L['D.Wealth'] = L['Wealth_next']- L['Wealth']

L.head()

| Wealth | Investment | value | value_Wealth | Wealth_next | shadow price | D.Wealth | |

|---|---|---|---|---|---|---|---|

| Wealth | |||||||

| 5.030779 | 5.030779 | 3.461913 | 17.923286 | 0.911808 | 5.030781 | 0.911808 | 1.397911e-06 |

| 5.272484 | 5.272484 | 3.679447 | 18.143387 | 0.909432 | 5.272485 | 0.909432 | 1.256542e-06 |

| 5.732233 | 5.732233 | 4.093221 | 18.560459 | 0.904912 | 5.732234 | 0.904912 | 9.876423e-07 |

| 6.365024 | 6.365024 | 4.662732 | 19.131111 | 0.898692 | 6.365024 | 0.898692 | 6.175332e-07 |

| 7.108914 | 7.108914 | 5.332233 | 19.796920 | 0.891380 | 7.108914 | 0.891380 | 1.824439e-07 |

Plotting the results¶

Optimal Policy¶

fig1, ax = plt.subplots()

ax.set(title='Optimal Investment Policy', xlabel='Wealth', ylabel='Investment')

ax.plot(S.Investment, label='Chebychev Collocation')

ax.plot(L.Investment, label='L-Q Approximation')

ax.plot(sstar, kstar,'wo')

ax.annotate(f"$s^*$ = {sstar:.2f}\n$k^*$ = {kstar:.2f}",[sstar, kstar],va='top')

ax.legend(loc= 'upper left');

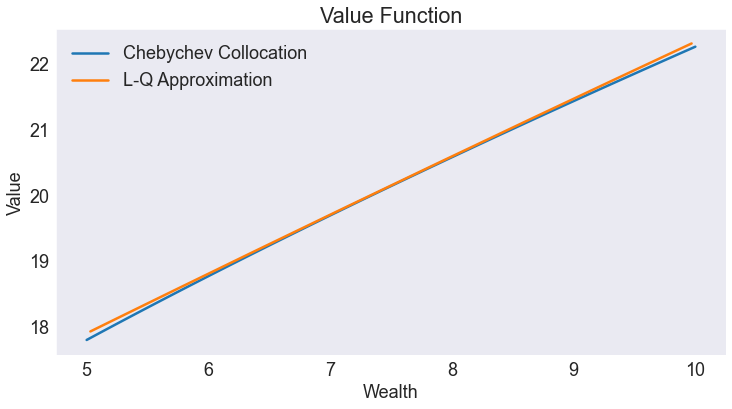

Value Function¶

fig2, ax = plt.subplots()

ax.set(title='Value Function', xlabel='Wealth', ylabel='Value')

ax.plot(S.value, label='Chebychev Collocation')

ax.plot(L.value, label='L-Q Approximation')

ax.legend(loc= 'upper left');

Shadow Price Function¶

fig3, ax = plt.subplots()

ax.set(title='Shadow Price Function', xlabel='Wealth', ylabel='Shadow Price')

ax.plot(S['shadow price'], label='Chebychev Collocation')

ax.plot(L['shadow price'], label='L-Q Approximation')

ax.legend(loc= 'upper right');

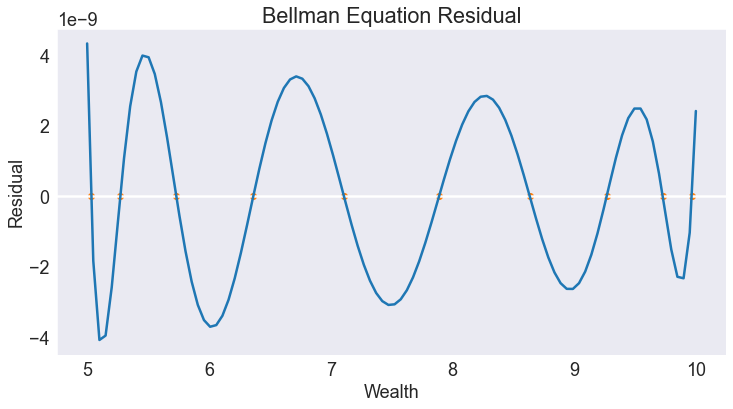

Chebychev Collocation Residual¶

fig4, ax = plt.subplots()

ax.set(title='Bellman Equation Residual', xlabel='Wealth', ylabel='Residual')

ax.axhline(0, color='w')

ax.plot(S[['resid']])

ax.scatter(basis.nodes[0], np.zeros_like(basis.nodes[0]), color='C1')

ax.ticklabel_format(style='sci', axis='y', scilimits=(-1,1))

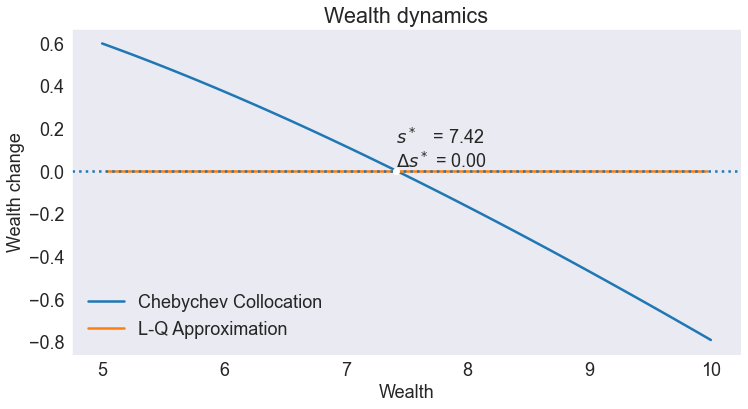

Wealth dynamics¶

Notice how the steady-state is stable in the Chebyshev collocation solution, but unstable in the linear-quadratic approximation. In particular, simulated paths of wealth in the L-Q approximation will converge to zero, unless the initial states is within a small neighborhood of the steady-state.

fig5, ax = plt.subplots()

ax.set(title='Wealth dynamics', xlabel='Wealth', ylabel='Wealth change')

ax.plot(S['D.Wealth'], label='Chebychev Collocation')

ax.plot(L['D.Wealth'], label='L-Q Approximation')

ax.axhline(0, linestyle=':')

ax.plot(sstar, 0, 'wo')

ax.annotate(f"$s^*$ = {sstar:.2f}\n$\Delta s^*$ = 0.00",[sstar, 0], va='bottom')

plt.legend(loc= 'lower left');

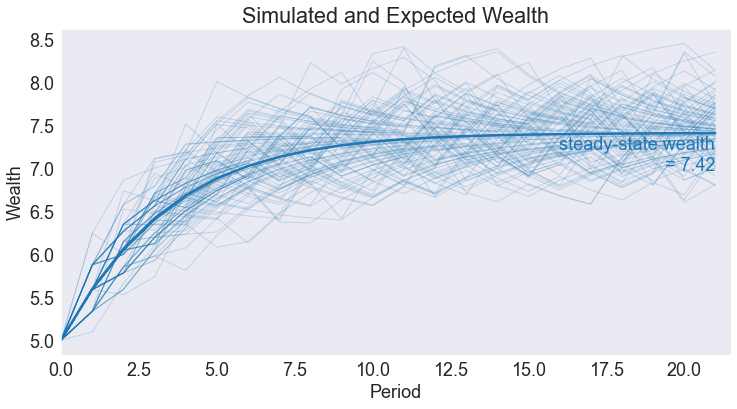

Simulating the model¶

We simulate 21 periods of the model starting from \(s=s_{\min}\)

T = 21

nrep = 50_000

data = growth_model.simulate(T, np.tile(smin,nrep))

Simulated State and Policy Paths¶

subdata = data.query('_rep < 100')

fig6, ax = plt.subplots()

ax.set(title='Simulated and Expected Wealth',

xlabel='Period',

ylabel='Wealth',

xlim=[0, T + 0.5])

ax.plot(data[['time','Wealth']].groupby('time').mean())

ax.plot(subdata.pivot('time','_rep','Wealth'), lw=1, color='C0', alpha=0.2)

ax.annotate(f'steady-state wealth\n = {sstar:.2f}', [T, sstar-0.03], color='C0', va='top', ha='right')

Text(21, 7.386897506925211, 'steady-state wealth\n = 7.42')

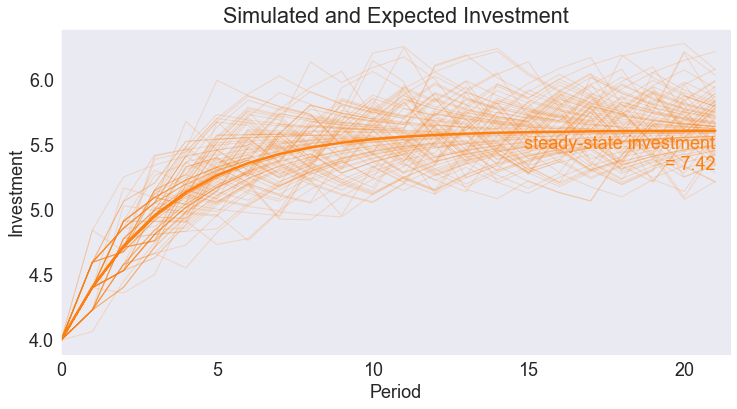

fig7, ax = plt.subplots()

ax.set(title='Simulated and Expected Investment',

xlabel='Period',

ylabel='Investment',

xlim=[0, T + 0.5],

xticks=range(0,T+1,5))

ax.plot(data[['time','Investment']].groupby('time').mean(), color='C1')

ax.plot(subdata.pivot('time','_rep','Investment'),lw=1, color='C1', alpha=0.2)

ax.annotate(f'steady-state investment\n = {sstar:.2f}', [T, kstar-0.03], color='C1', va='top', ha='right')

Text(21, 5.579418282548479, 'steady-state investment\n = 7.42')

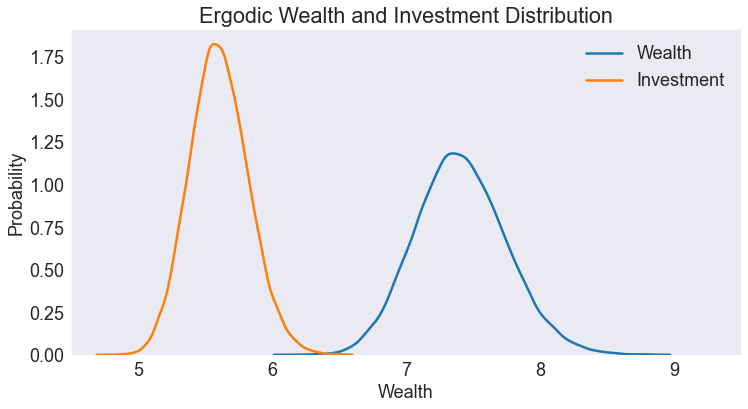

Ergodic Wealth Distribution¶

data.query("time == @T")

| time | _rep | Wealth | Investment | |

|---|---|---|---|---|

| 1050000 | 21 | 0 | 7.316155 | 5.544752 |

| 1050001 | 21 | 1 | 7.340926 | 5.560817 |

| 1050002 | 21 | 2 | 7.582651 | 5.717136 |

| 1050003 | 21 | 3 | 7.236199 | 5.492836 |

| 1050004 | 21 | 4 | 7.489982 | 5.657305 |

| ... | ... | ... | ... | ... |

| 1099995 | 21 | 49995 | 7.827284 | 5.874527 |

| 1099996 | 21 | 49996 | 7.302025 | 5.535583 |

| 1099997 | 21 | 49997 | 7.833176 | 5.878308 |

| 1099998 | 21 | 49998 | 7.309855 | 5.540664 |

| 1099999 | 21 | 49999 | 7.911989 | 5.928839 |

50000 rows × 4 columns

subdata = data.query("time == @T")[['Wealth','Investment']]

stats =pd.DataFrame({'Deterministic Steady-State': [sstar, kstar],

'Ergodic Means': subdata.mean(),

'Ergodic Standard Deviations': subdata.std()}).T

stats

| Wealth | Investment | |

|---|---|---|

| Deterministic Steady-State | 7.416898 | 5.609418 |

| Ergodic Means | 7.410732 | 5.605236 |

| Ergodic Standard Deviations | 0.339563 | 0.219709 |

fig8, ax = plt.subplots()

ax.set(title='Ergodic Wealth and Investment Distribution',

xlabel='Wealth',

ylabel='Probability',

xlim=[4.5, 9.5])

sns.kdeplot(subdata['Wealth'], ax=ax, label='Wealth')

sns.kdeplot(subdata['Investment'], ax=ax, label='Investment')

ax.legend();